Yale 360 notes:

The cost of manufacturing solar panels is dropping more quickly than previously predicted, putting solar energy on course to meet 20 percent of global energy demand by 2027, according to Oxford University mathematicians, who developed a new forecasting model. By contrast, the International Energy Agency’s predictions are far more conservative, stating that by 2050, solar panels will generate just 16 percent of global energy demand. The Oxford researchers' model predicts solar panel costs will continue to decrease 10 percent a year for the foreseeable future. Their model draws on historical data from 53 different technologies.... said Oxford's Doyne Farmer, who co-wrote the paper. “We put ourselves in the past, pretended we didn’t know the future, and used a simple method to forecast the costs of the technologies,” he said.

...

Highlights

• A generalized version of Moore's law for unit costs is modelled as a correlated geometric random walk with drift.

• We study 53 technologies from different sectors.

• We model forecast errors and empirically test hypotheses about predictability.

• We apply our method to make forecasts for the price of photovoltaic modules.

Abstract:

Recently it has become clear that many technologies follow a generalized version of Moore's law, i.e. costs tend to drop exponentially, at different rates that depend on the technology. Here we formulate Moore's law as a correlated geometric random walk with drift, and apply it to historical data on 53 technologies. We derive a closed form expression approximating the distribution of forecast errors as a function of time. Based on hind-casting experiments we show that this works well, making it possible to collapse the forecast errors for many different technologies at different time horizons onto the same universal distribution. This is valuable because it allows us to make forecasts for any given technology with a clear understanding of the quality of the forecasts. As a practical demonstration we make distributional forecasts at different time horizons for solar photovoltaic modules, and show how our method can be used to estimate the probability that a given technology will outperform another technology at a given point in the future.

...

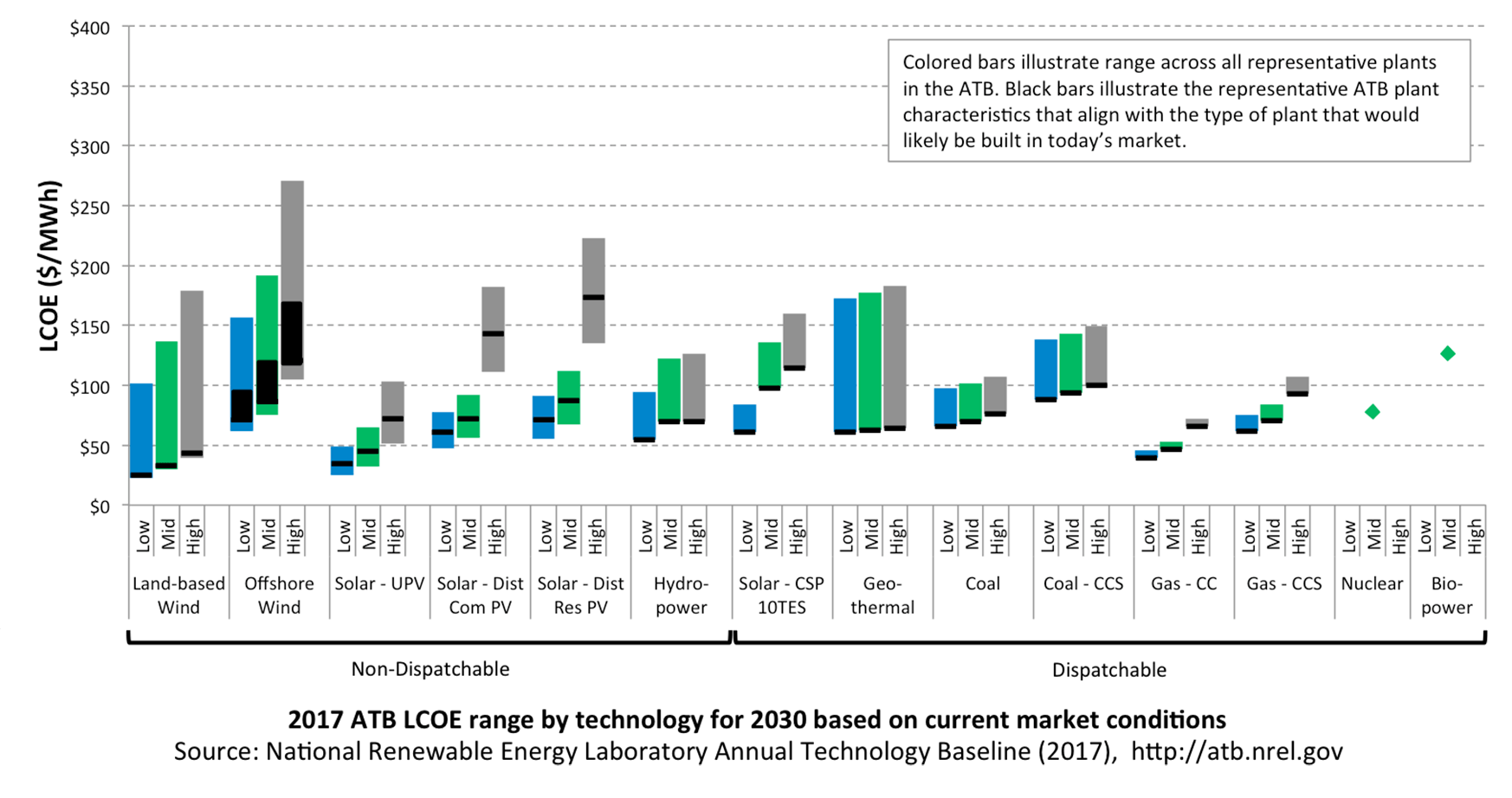

Over the last 150 years the inflation-adjusted price of coal has fluctuated by a factor of three or so, but shows no long term trend, and indeed from the historical time series one cannot reject the null hypothesis of a random walk with no drift2 (McNerney et al., 2011). Nuclear power and solar photovoltaic electricity, in contrast, are both new technologies that emerged at roughly the same time. The first commercial nuclear power plant opened in 1956 and the first practical use of solar photovoltaics was as a power supply for the Vanguard I satellite in 1958. The cost of electricity generated by nuclear power is highly variable, but has generally increased by a factor of two or three during the period shown here. In contrast, a watt of solar photovoltaic capacity cost $256 in 1956 (Perlin, 1999) (about $1910 in 2013 dollars) vs. $0.82 in 2013, dropping in price by a factor of about 2330. Since 1980 photovoltaic modules have decreased in cost at an average rate of about 10% per year.

The prediction says that it is likely that solar PV modules will

continue to drop in cost at the roughly 10% rate that they have in the

past. Nonetheless there is a small probability (about 5%) that the price

in 2030 will be higher than it was in 2013.

...

An analysis of coal-fired electricity, breaking down costs into their

components and examining each of the trends separately, has been made by

McNerney et al. (2011).

They show that while coal plant costs (which are currently roughly 40%

of total cost) dropped historically, this trend reversed circa 1980.

Even if the recent trend reverses and plant construction cost drops

dramatically in the future, the cost of coal is likely to eventually

dominate the total cost of coal-fired electricity. As mentioned before,

this is because the historical cost of coal is consistent with a random

walk without drift, and currently fuel is about 40% of total costs. If

coal remains constant in cost (except for random fluctuations up or

down) then this places a hard bound on how much the total cost of

coal-fired electricity can decrease. Since typical plants have

efficiencies the order of 1/3 there is not much room for making the

burning of coal more efficient – even a spectacular efficiency

improvement to 2/3 of the theoretical limit is only an improvement of a

factor of two, corresponding to the average progress PV modules make in

about 7.5 years. Similar arguments apply to oil and natural gas.

Because historical nuclear power costs have tended to increase, not just

in the US but worldwide, even a forecast that they will remain constant

seems optimistic. Levelized costs for solar PV powerplants in 2013 were

as low as 0.078–0.142 Euro/kWh (0.09–0.16$) in Germany (

Kost et al., 2013),

27 and in 2014 solar PV reached a new record low with an accepted bid of $0.06/kWh for a plant in Dubai.

28

When these are compared to the projected cost of $0.14/kWh in 2023 for

the Hinkley Point nuclear reactor, it appears that the two technologies

already have roughly equal costs, though of course a direct comparison

is difficult due to factors such as intermittency, waste disposal,

insurance costs, etc.

...

As a final note, skeptics

have claimed that solar PV cannot be ramped up quickly enough to play a

significant role in combatting global warming. A simple trend

extrapolation of the growth of solar energy (PV and solar thermal)

suggests that it could represent 20% of the energy consumption by 2027.

In contrast the “hi-Ren” (high renewable) scenario of the International

Energy Agency, which is presumably based on expert analysis, assumes

that PV will generate 16% of total electricity in 2050. Thus even in

their optimistic forecast they assume PV will take 25 years longer than

the historical trend suggests (to hit a lower target).

by J. Doyne Farmer 1, 2 and 3, , François Lafonda, 1, 4 and 5

1. Institute for New Economic Thinking at the Oxford Martin School, University of Oxford, Oxford OX2 6ED, UK

2. Mathematical Institute, University of Oxford, Oxford OX1 3LP, UK

3. Santa-Fe Institute, Santa Fe, NM 87501, USA

4. London Institute for Mathematical Sciences, London W1K 2XF, UK

5. United Nations University – MERIT, 6211TC Maastricht, The Netherlands

Research Policy via Elsevier Science Direct

www.ScienceDirect.com

Volume 45, Issue 3; April, 2016; Pages 647–66; Available online 6 January 2016

Keywords: Forecasting; Technological progress; Moore's law; Solar energy

.png)